Quick Commerce, Dark Stores & Logistics-Tech: Convergence of Wealth Creation?

5 min read

Is Quick Commerce the future of commerce? Will we see India’s first Logistics-Tech unicorn in 2022? Need to throw some light on ‘Dark Stores’? Let’s quickly dive in..

The model is primarily is based on 3 pillars:

- Can you complete an ‘essential item’ transaction in ~10 mins? (buying offline might take even 30-40 mins, so here’s selling your time back to you on an app).

- Product offerings that are sharp, and well-assorted on a daily/weekly basis. These might even be customized for each, using user data analytics.

- Making unit-economics work as they operate on wafer-thin profit margins.

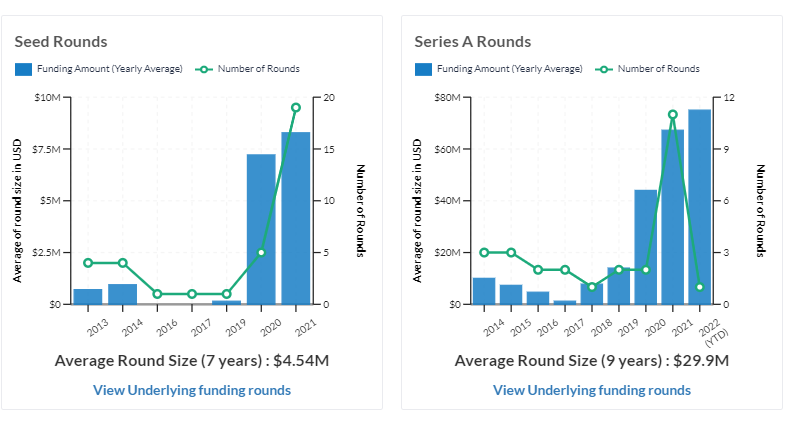

India’s ‘Consumables market’ is projected to touch ~$1 Trillion by 2025 from ~$725 billion in 2020. Currently, Q-commerce is a $300 million market as of 2021, and this sub-sector within the consumables market is expected to grow >15x in 4 years to reach $5 billion by 2025 – as per RedSeer report. Platforms like Swiggy’s Instamart, Zomato backed Binkit, Zepto, and Reliance-backed Dunzo aim to expand their foothold in this hot emerging sector. Here’s a look at ‘Global funding trends in the Quick-Commerce sector’ across ‘Seed to Series C’ stage investments over recent years (Source: Tracxn):-

In Dec’21, $100 million fund infusion in the one-year-old Indian startup Zepto at a $570 million valuation (founded by a 19-year-old Stanford dropout). Zepto is adding nearly 1 lakh new customers per week and has 100+ dark stores (mini-warehouses that cater only to online shoppers) across locations.

While conventional E-groceries manage close to 100K SKUs, ‘dark stores’ focus on a set of ~2K SKUs. For example, Blinkit (previously Grofers) has more than 350 dark stores for Q-commerce to deliver orders within 10-30 mins. Indian consumers love it and that is why there is a 50% average weekly retention, which means half of the users come back next week itself and consistently keep coming back.

- Swiggy also plans to invest $700M in Instamart to scale up non-food delivery categories.

- BigBasket is considering its own 10-min delivery service through Tata Group’s super-app Tata Neu.

- Social commerce firm Meesho (now turned Amazon competitor in India) is also offering free home deliveries on food and grocery orders in non-Tier 1 towns.

- ‘DMart Ready’ and ‘JioMart’ have been offering some of the highest discounted rates on essentials which are currently unmatched by Q-commerce.

Globally, this Q-commerce model found huge traction in evolved markets like the US and European countries. Few Q-commerce startups in Europe operating in this space include UK-based Dija, Jiffy, and Zapp, and Germany-based Flink and Gorillas.

Gorillas became the fastest European unicorn after their $290M fundraise in 2021. In China, too, companies such as Miss Fresh, Meituan Maicai, and Dingdong Maicai are competing with giant players like Alibaba, JD, and Pinduoduo for their market share in the $400 billion online Chinese grocery space.

The first key paradigm shift is in the psychological behavior of consumers. Indian consumers are turning from ‘value seeking’ to more ‘convenience seeking’ by ordering weekly and in small quantities. Along with aggressively acquiring customers, they are altering the customer behavior of the masses! For example, A pop-up led last-minute add-on product during checkout, paying using a specific card/wallet for discount & offers, or even ‘Buy Now Pay Later’ trend alongside unique offers/bundled purchases at steep discounts + all now reach you in 10 minutes!

As per reports, the average order value is nearly Rs. 400-700 depending on the location. To break even on the unit economics a dark store needs to do 1000-1200 orders per day. Wherein, the gross margins are 22-25% and operating margins are around 5-7%. The market opportunity across Indian cities is as below (Sources: Redseer, India Research, Philip Capital) -:

Next, the setting up of micro-warehouses located closer to the point of delivery and restricting their SKUs focussed 2,000 high-demand items. Real estate giant JLL defines these ‘dark stores’ as ‘urban logistics spaces’. According to a report it released in 2021, India is expected to witness a demand for an additional 7 million sq ft of in-city warehouse space by 2022 across tier-1 and tier-2 cities. “While the tier-1 cities are expected to receive most of the planned growth demand of approximately 5 million sqft, several tier-2 cities like Jaipur, Lucknow, Kochi, Surat, Vizag, Vijayawada, Nagpur, and Guwahati are witnessing increased attention,” the report says.

The hyped macro trends have been a game-changer in traditional logistics and SaaS logistics spaces. Indian logistics is currently a $250 billion sector and is estimated to grow at 10%-12% CAGR. ‘Total Logistics Spend’ contributes to ~14% of the overall GDP of India! Logistics-Tech company Shadowfax serviced 6 lakh quick commerce orders daily in January 2022, as compared to only 1 lakh orders a day in January 2021 – seeing a 500% growth rate! Other leading Indian SaaS-Logistics players include Shiprocket, Shipsy, Locus, Pickrr, FarEye and more.

Lastly, the use of individual consumer order data sets with AI and ML to provide end-to-end smart SaaS-logistics + efficient Dark store inventory tracking becomes critical to reduce customer complaints by ~28% as per reports. Real-time tech tools combine and assign the correct order to the correct dark store, 6-second packing once the order is placed on the app, automatic geospatial route mapping with nearest delivery resources – all to finally deliver within 10 minutes.

Now, the recipe of a successful unicorn has two primary special ingredients – the funds and the talent. We all know, big cheques have been pouring for these start-ups, so expansion cash burns are taken care of. However, building strong leadership teams is equally critical to driving these rocketships’ growth. And to everyone’s surprise, even the Top talent from India’s giant unicorn startups have been flowing into these quick commerce core teams as quickly as the funding and deliveries. For example, Zepto has hired experienced senior leaders from Flipkart, Uber, Dream11, PharmEasy, and Pepperfry!

To conclude, encouraged by successful IPOs in 2021, notably those of Zomato and Nykaa, 71% of Indian startup founders believe that an IPO is the likely mode of exit for investors. This is a significant increase over 2020 when only 47% of founders held that view as per industry reports. Other favorable trends helping increase digital commerce penetration include :

- $970 Bn worth of UPI transactions in 2021, a year-on-year rise of over 110%!

- Global influencer market at a record $13.8 billion, with 46% of marketing professionals planning to increase influencer marketing investments in 2022.

- India’s average age is 26-30, with over ~500 million young millennials open to experimenting and adapting quickly to new innovative apps and tech products.

- With low-cost internet and the 760 million Indian internet users (that saw a growth explosion after 2016), are currently equal to the population of the whole of Europe and are still steadily growing!

As more unused cinemas and marriage, halls turn into dark stores for quick commerce, and SaaS logistics strengthens their deep-tech with exploding order data volumes and AI analytics – the Indian quick commerce sector is evidently a silver-lining game changer for the Indian retail industry and consumers of the 21st century.

Written by: Nihal, Harsh, and Rony